What a $50 Million New York Fraud Scheme Reveals About California’s Ballot Initiative

A federal indictment unsealed in Manhattan in March 2026 details an organized auto insurance fraud scheme that submitted tens of millions in fraudulent medical claims to New York insurers. The case raises legitimate questions, but not necessarily the ones being cited to justify California’s ballot initiative.

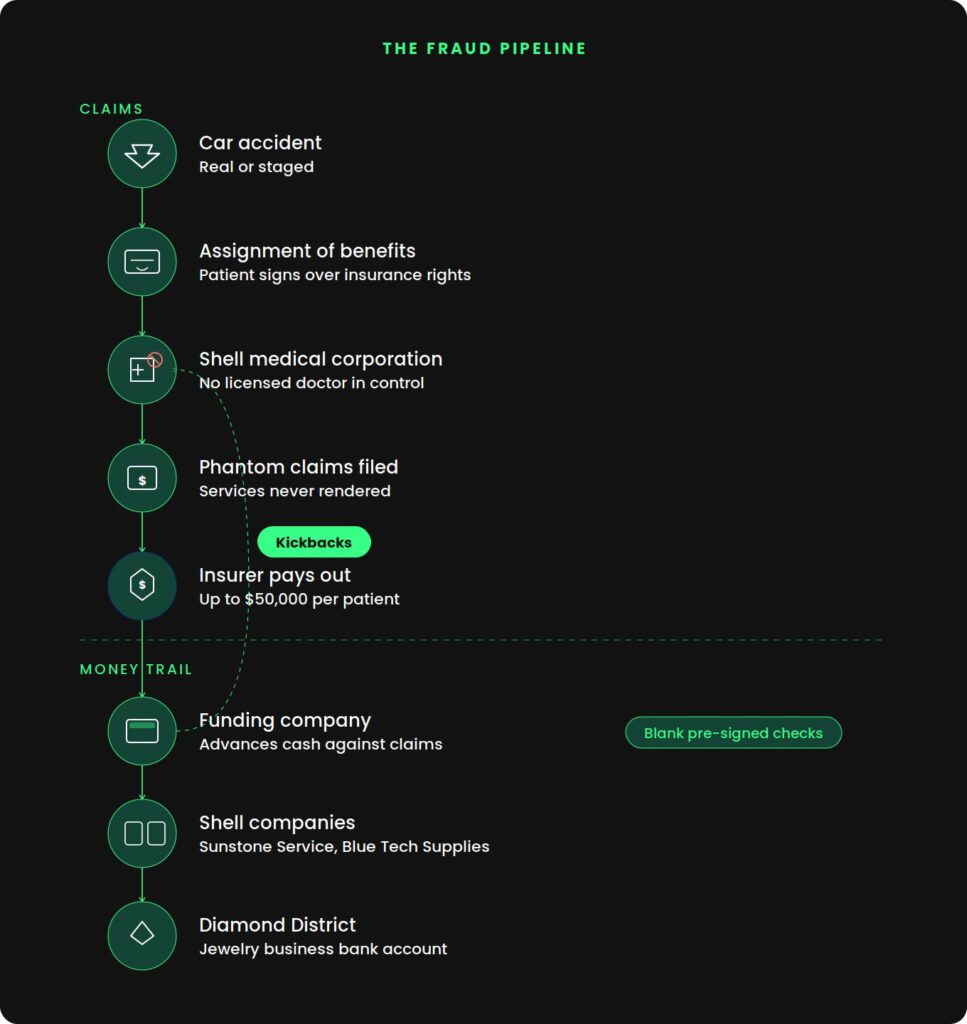

A restaurateur who ran one of Manhattan’s most connected nightlife spots. A funding company operated by the former mayor’s chief of staff. Shell medical corporations staffed by doctors who never treated a single patient. Blank, pre-signed checks filled out in the defendant’s presence. Millions were laundered through a jewelry business in the Diamond District.

And at the center of it all: car insurance claims.

On March 31, 2026, the U.S. Attorney for the Southern District of New York unsealed an indictment charging Zhan Petrosyants, a 44-year-old restaurateur known as ‘Johnny,’ with conspiracy to commit healthcare fraud, wire fraud, aggravated identity theft, and money laundering. The scheme ran from 2018 to 2023 and submitted tens of millions of dollars in fraudulent medical claims to New York auto insurers.

Petrosyants is not a lawyer or a medical professional. He co-owned a Manhattan restaurant and, according to prosecutors, used shell medical corporations and co-conspirators to submit fraudulent claims through New York’s no-fault insurance system.

The case has drawn attention beyond New York. The same corporation spending $32.5 million on California’s Initiative 25-0022 has cited cases like this one to build public support for similar reforms in multiple states. That connection is worth examining – because the mechanics of how the Petrosyants scheme worked reveal important differences between the fraud being cited and the system the initiative would actually change.

How the Scheme Worked

The Petrosyants indictment is a textbook example of no-fault insurance fraud, a category of crime that thrives in states where the system is designed to pay medical claims quickly and without assigning blame.

New York requires every registered vehicle to carry no-fault insurance under Insurance Law Article 51, providing up to $50,000 per person in medical benefits regardless of who caused the accident. Patients can sign an “assignment of benefits” form, which transfers their right to insurance reimbursement directly to a medical provider. The provider then bills the insurer, collects payment, and the patient never touches the money.

That assignment mechanism is the vulnerability. Petrosyants and his co-conspirators exploited it by setting up medical corporations that appeared to be owned by licensed professionals but were actually controlled by non-medical operators. They recruited doctors and psychologists whose names, license numbers, and signatures were placed on billing records for treatments that were either never provided or medically unnecessary. They submitted those bills directly to auto insurers through the assignment pipeline. And they accelerated their access to cash by routing claims through a funding company that advanced money against pending insurance payouts.

That funding company has been identified in court filings and reporting as Finance Vision Capital Group, an entity connected to Frank Carone, Adams’ former chief of staff and a powerful Brooklyn political operative. Carone’s lawyers maintain that Finance Vision is a “victim” of the fraud. But emails filed in a related GEICO civil racketeering lawsuit show direct contacts between Carone’s firm and all three defendants, including communications about recruiting doctors and concerns about claims that appeared to be “not justified by their medical records.”

The proceeds were laundered through two shell corporations, Sunstone Service Inc. and Blue Tech Supplies Inc. (neither a medical provider), then transferred to a bank account held by a jewelry business in Manhattan’s Diamond District. Some kickback payments were delivered via blank, pre-signed checks drawn on accounts nominally controlled by the sham medical providers. This wasn’t Petrosyants’ first run. In 2014, he and his twin brother Robert pleaded guilty to Bank Secrecy Act violations in a check-cashing scheme tied to the same type of no-fault claims.

Why This Kind of Fraud Thrives in New York

The Petrosyants case isn’t an anomaly. It’s a product of system design.

No-fault states have consistently higher auto insurance fraud rates than at-fault states. The Insurance Research Council found that fraud and claim buildup added $5.6 to $7.7 billion in excess payments across U.S. auto injury claims, and the problem was “more pervasive in no-fault insurance states.” Florida and New York led the pack. The three most expensive states for auto insurance in America, Michigan, New York, and New Jersey, are all no-fault states. When Colorado repealed its no-fault law in 2003 and switched to a tort system, premiums dropped 35% within five years.

The reason is structural. In no-fault states, the assignment of benefits creates a direct billing channel from provider to insurer with minimal scrutiny. Insurers must pay promptly. The patient is removed from the financial equation entirely. For organized fraud rings, this created a straightforward pipeline: establish a shell clinic, submit bills for phantom services, and collect payment before insurers could scrutinize the claims.

Why This Can’t Happen the Same Way in California

California is not a no-fault state. It’s an at-fault tort state with a pure comparative negligence system. There is no assignment of benefits. There is no $50,000 PIP pool that providers can tap directly.

When someone is injured in a car accident in California, the process works differently at every step. Medical providers who treat accident victims typically do so on a lien, meaning they agree to defer payment until the case settles or goes to judgment. The provider bears the risk that the case might not pay out. Before any money changes hands, there’s an attorney negotiating, an insurance adjuster contesting, and often a court reviewing the claim. The pipeline that Petrosyants exploited, where a clinic can bill an insurer directly and collect without any litigation or settlement, simply doesn’t exist here.

California’s fraud concerns are real but structurally different. The risk in a lien-based system is inflated billing designed to boost settlement values, not phantom clinics billing for services never rendered. And California already has a criminal statute targeting the kickback side of that equation. Business & Professions Code § 650 prohibits any licensed healthcare provider from offering or accepting compensation for patient referrals, with violations carrying up to three years in prison and a $50,000 fine. California’s Department of Insurance Fraud Division made 272 arrests in FY 2023-24 and identified over $207 million in potential fraud losses. The enforcement infrastructure exists and is actively being used.

The Ballot Initiative That Claims to Fix a Problem California Doesn’t Have

This is where the story pivots from New York to your ballot.

Initiative 25-0022, the “Protecting Automobile Accident Victims from Attorney Self-Dealing Act,” is backed by Uber with $32.5 million in funding and is currently gathering signatures for the November 2026 ballot. It proposes capping attorney fees at 25% of total recovery, limiting recoverable medical expenses to 125% of Medicare reimbursement rates, imposing a heightened “clear and convincing evidence” standard for unpaid medical bills, and prohibiting certain attorney-provider financial arrangements.

Examining each provision against the mechanics of the Petrosyants scheme reveals both where the initiative addresses genuine concerns and where its reach extends beyond the fraud being cited to justify it.

The fee cap targets contingency-fee attorneys. Petrosyants didn’t use attorneys to submit his fraudulent claims. He used shell medical corporations and blank checks. A fee cap would not have slowed him down for a second.

The Medicare rate caps limit what victims can recover for legitimate medical treatment. Petrosyants billed for services that were never rendered. The billing amount was irrelevant because the treatments were fictional. Rate caps can’t stop phantom billing. What they can do is discourage real doctors from treating real accident victims on liens, because the recoverable amount won’t cover the cost of care.

The heightened burden of proof applies in civil litigation. Organized fraud rings like the one Petrosyants ran don’t litigate in court. They submit claims directly to insurers through the no-fault pipeline and cash out through funding companies. This evidentiary standard change is invisible to criminal enterprises. It only affects legitimate plaintiffs trying to recover actual medical costs.

The anti-kickback provision is the one element that touches a genuine concern. But California’s BPC § 650 already covers this ground. The initiative would elevate its version to constitutional status, making it nearly impossible to amend if it produces unintended consequences.

The Legislative Analyst’s Office has projected that if the initiative passes, attorneys would decline economically unviable cases, reducing the number of filings. Medi-Cal costs would increase by millions to tens of millions annually as victims shift to public programs. The measure doesn’t reduce fraud. It reduces access.

The Same Playbook, Two States, One Funder

The connection between New York and California isn’t just thematic. It’s organizational.

Protecting American Consumers Together (PACT), an advocacy group backed in part by Uber, launched in 2025 with a $10 million budget and is operating in at least four states simultaneously. In California, PACT endorsed Initiative 25-0022. In New York, PACT ran a seven-figure TV ad campaign targeting “billboard lawyers” in support of Governor Hochul’s insurance reforms. The language is identical across both campaigns: lawsuit abuse, predatory attorneys, and consumer protection.

The Petrosyants indictment landed in the middle of Hochul’s push for reform. Insurance industry allies immediately cited it as justification. But here’s the disconnect that should give every voter pause: 70% of suspected auto insurance fraud in New York is related to no-fault claims, according to the state’s own data. Hochul’s major proposals don’t touch the no-fault system. They target tort law, restricting pain-and-suffering lawsuits. The fraud is no-fault. The reform is tort. The beneficiaries are insurers and companies like Uber that face tort liability.

In California, the same pattern holds. Uber cites fraud and “self-dealing” to justify an initiative that caps victim recoveries and attorney fees. But California’s at-fault system doesn’t have the structural vulnerability that produced the Petrosyants scheme in the first place.

The parallel campaigns in California and New York — using similar language and backed by overlapping funding sources — raise questions about whether the proposed reforms are designed to address fraud specifically or to reduce liability exposure more broadly.

The Fraud Is Real. So Is the Misdirection.

Nobody should look at the Petrosyants indictment and conclude that auto insurance fraud isn’t a serious problem. It is. Federal prosecutors allege tens of millions in fraudulent claims, laundered through shell companies and a Diamond District jewelry business, connected to one of the most politically wired networks in New York City. That’s organized crime exploiting a broken system.

But a constitutional amendment that caps what injured Californians can recover for medical treatment doesn’t stop a restaurateur from setting up a fake medical corporation in Manhattan. It doesn’t shut down a funding company that advances cash against phantom claims. It doesn’t prevent blank checks from being filled out in a co-conspirator’s presence.

What it does is make sure that when a real person gets hurt in a real car accident on a California freeway, the system designed to help them would look significantly different – with fewer attorneys willing to take their case, fewer doctors willing to treat them on a lien, and lower recoveries when they do get to court. The change could also increase Medi-Cal costs for California taxpayers as more victims fall back on public programs.

The fraud documented in New York is real and worth prosecuting. The more consequential question for California voters is whether the reforms being proposed are calibrated to address the same problem – or whether they address a different problem entirely, with different beneficiaries.

If someone asks you to sign a petition for the “Protecting Automobile Accident Victims from Attorney Self-Dealing Act,” remember what you just read. Then ask yourself who that title is actually designed to protect.

What could your case be worth?

Get a quick estimate in under 2 minutes

Explore lo que más le importa

Buscando por ubicación o tipo de caso, le ayudaremos a llegar exactamente a donde necesita.

Ubique nuestra oficina más cercana.

Navegue por todas las ciudades y condados que atendemos. Vea en qué lugares nuestros abogados triunfan todos los días.

Explore las áreas de enfoque legal

Desde accidentes automovilísticos hasta demandas por muerte por negligencia, conozca todos los tipos de casos que manejamos con confianza.

En DK Law estamos a su lado — all the way.

¡Agende hoy su consulta gratuita con nuestros expertos!

El tiempo es importante después de un accidente

Cuanto antes hables con un abogado después de un accidente, más sólido puede ser su reclamo. Actuar pronto ayuda a preservar la evidencia y a proteger sus derechos.

No ganamos, no cobramos | Disponible 24/7