Can I Sue My Insurance Company for Emotional Distress? Yes, but…

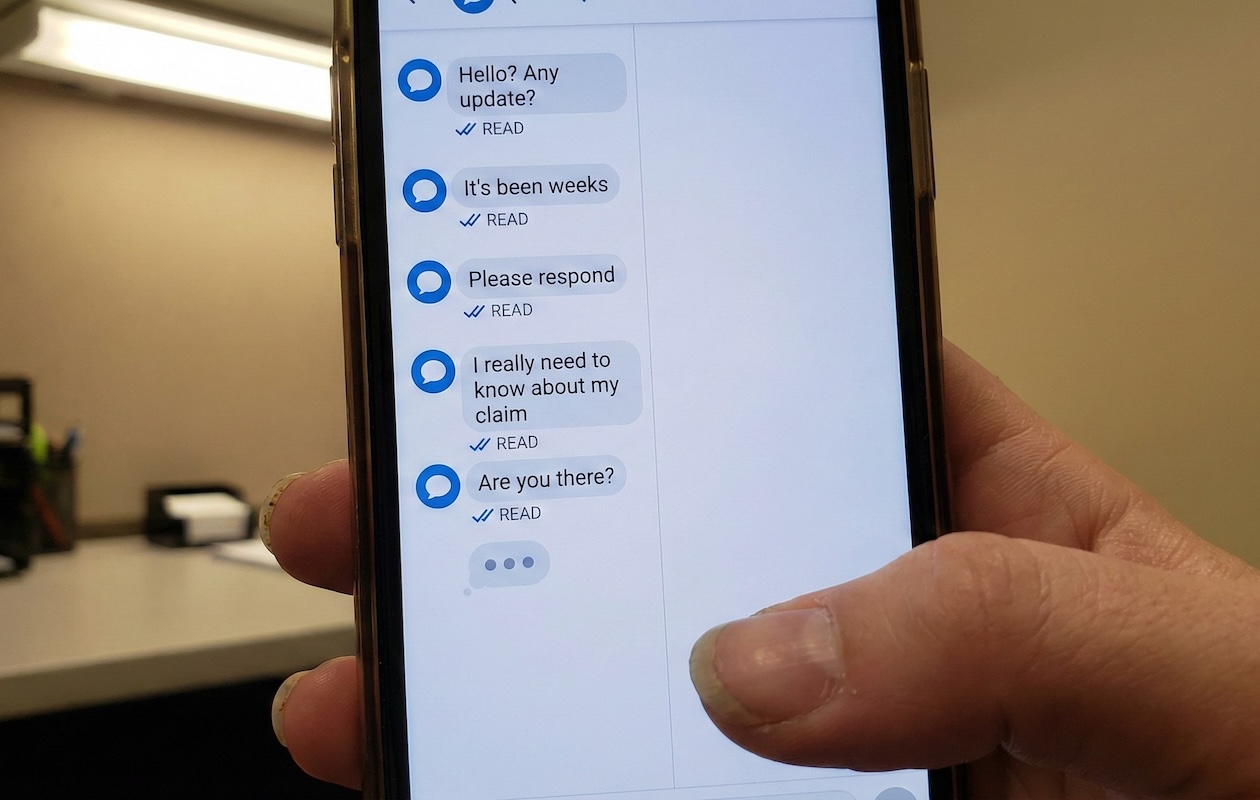

You survive the crash. That was supposed to be the hard part. But months later, you realize the accident was just the beginning. Now you’re dealing with the “Second Injury.” The sleepless nights, the panic attacks, and the financial terror caused by an insurance adjuster who treats you like a criminal instead of a victim.

You want to know if you can make them pay for the stress they are causing you.

The short answer is yes, but it depends entirely on which insurance company you are targeting.

The law treats your own insurance company differently from the other driver’s company. One owes you a duty of care. The other is legally allowed to act like your enemy. Understanding this distinction is the only way to turn your frustration into a winning legal strategy.

Conclusiones principales

- Know Your Enemy: You generally cannot sue the at-fault driver’s insurance company for bad faith because they have no contract with you.

- The Exception: Si puede - sue your own insurance company (for Uninsured Motorist or MedPay claims) if they unreasonably delay or deny your claim.

- The “Bad Faith” Tool: California law allows you to recover damages specifically for the emotional distress caused by an insurer’s financial abuse, separate from your physical injuries.

- The High Bar: Proving “Intentional Infliction of Emotional Distress” requires showing the conduct was “outrageous,” not just rude.

The Two Types of Emotional Distress Claims in California

Most people, and frankly, many inexperienced lawyers, confuse two very different legal concepts. If you go into a consultation mixing these up, you might be told you have no case when you actually do.

You need to separate the suffering caused by the accidente from the suffering caused by the insurance company.

- Pain and Suffering (Standard): This is compensation for the anxiety, PTSD, and depression caused by the car crash itself. This is a standard part of every personal injury settlement.

- Bad Faith Damages (The Lawsuit): This is compensation for the anxiety caused by the claims process. This happens when the insurance company drags its feet, lies to you, or denies a valid claim to save money.

We are talking about the second one here. This isn’t about a broken bone. It’s about a broken promise.

Scenario A: Suing the At-Fault Driver’s Insurance (Third-Party Claims)

If another driver hits you, and their insurance company (say, State Farm or Geico) is being incredibly rude to you, delaying your check, or ignoring your calls… You generally cannot sue the insurance company directly for that behavior.

Why? Because you don’t have a contract with them. You aren’t their customer.

In California, a legal doctrine established by the Supreme Court case Moradi-Shalal v. Fireman’s Fund Ins. Companies effectively block victims from suing a third-party insurer for “Bad Faith.” The law views the insurance adjuster as your adversary. Their job is to protect their driver, not you. They are allowed to fight you.

The Workaround

Just because you can’t sue the company for their bad behavior doesn’t mean they get away with it. When an adjuster acts aggressively, we use that against them to increase the value of your Dolor y Sufrimiento (General Damages) claim against their driver.

Según California Civil Code § 3333, you are owed compensation for all damages caused by the accident. If the insurance company drags out the process, forcing you into financial desperation, you can argue that this exacerbated your emotional distress. We make the insurance company pay for the misery their delay tactics created, just under a different label.

Scenario B: Suing Your Own Insurance Company (First-Party Claims)

This is where the game changes completely.

If you are filing a claim with your own insurance company, they cannot treat you like an enemy. You paid your premiums. You have a contract.

In California, every insurance policy contains an “Implied Covenant of Good Faith and Fair Dealing.”

The California Supreme Court ruled in Egan v. Mutual of Omaha Insurance Co. that an insurer must give at least as much consideration to your interests as they do to their own. If they don’t, they are breaking the law.

If your own insurer unreasonably delays or denies your claim, you can sue them for Bad Faith. This allows you to recover damages for:

- The contract benefits they owe you.

- Attorney fees to force them to pay.

- Angustia emocional specifically caused by their financial abuse.

- Punitive damages (in extreme cases).

What Does Bad Faith Look Like?

It’s rarely as obvious as an adjuster screaming at you. In 2025, it’s usually bureaucratic silence. According to California Insurance Code § 790.03(h), the following behaviors are illegal:

- Misrepresenting facts or policy provisions to you.

- Failing to acknowledge and act reasonably promptly upon communications.

- Failing to provide a prompt explanation for a denial.

- Lowballing: Attempting to settle a claim for less than the amount that a reasonable person would believe they were entitled to.

Signs You Have a Valid “Intentional Infliction of Emotional Distress” Case

Sometimes, the conduct is so bad that it goes beyond simple “Bad Faith” and enters the realm of “Intentional Infliction of Emotional Distress” (IIED). This is a separate tort claim you can file against the adjuster personally or the company.

However, be warned: the legal bar here is incredibly high.

To win an IIED claim, you must prove the conduct was “extreme and outrageous.” It has to be conduct that goes beyond all possible bounds of decency. Being rude isn’t enough. Being slow isn’t enough.

Courts have found “outrageous conduct” in cases where:

- An insurer rescinded a health policy to avoid paying for life-saving surgery while the patient was in the hospital (see Hailey v. California Physicians’ Service).

- Investigators stalked the victim’s family to intimidate them into dropping a claim.

- Adjusters used racial slurs or threats of physical violence.

Most of the time, we don’t need to prove this high standard. We stick to “Bad Faith” because, under cases like Gruenberg v. Aetna Insurance Co., you can recover emotional distress damages just by proving they were unreasonable. You don’t have to prove they were “evil” or “outrageous.”

The New Threat: AI and Automatic Denials

You might feel like you are being ignored by a human, but increasingly, you are being denied by a machine.

Recent class action lawsuits have revealed that major insurers are using algorithms to deny claims in bulk. For instance, reports indicate some systems allow doctors to deny claims in an average of 1.2 seconds without ever opening the patient’s medical file.

This is a massive frontier in Bad Faith law. California law requires a “thorough, fair, and objective” investigation. If an AI denies your claim based on a statistical average rather than your actual medical records, that is a textbook failure to investigate.

If you received a denial letter that feels generic or arrived suspiciously fast, an algorithm likely made the decision. That is not a valid investigation, and we can fight it.

How Much Compensation Can You Get for Emotional Distress?

If we successfully prove your own insurance company acted in Bad Faith, the potential compensation goes far beyond your medical bills.

Contract Damages:

First, they have to pay what they owed you originally (the surgery costs, the car repairs).

Emotional Distress Damages:

You can be compensated for the anxiety, insomnia, humiliation, and mental suffering caused by the delay. There is no cap on this. If their refusal to pay caused you to lose your home or miss a critical surgery, the jury can award significant money for that suffering.

Daños Punitivos:

This is the big one. If we can prove the insurer acted with “oppression, fraud, or malice” under California Civil Code § 3294, the jury can award Punitive Damages. These are not designed to pay you back; they are designed to punish the multi-billion dollar corporation so they don’t do it again.

Why You Need a Lawyer Who Isn’t Afraid of Trial

Insurance companies are essentially giant risk-calculation machines. They know which law firms simply process paperwork and which ones are willing to file a Bad Faith lawsuit and go to trial.

If you hire a “settlement mill” firm, the insurer knows they can lowball you. They know that the firm won’t put in the work to prove Bad Faith.

But when you hire a litigator, the calculation changes. The insurer has to ask: “Is saving $20,000 on this claim worth risking a $2 million Bad Faith verdict?”

Suddenly, they start returning calls. Suddenly, the check is in the mail.

¿Tengo un caso?

If you are wondering if your frustration is legally actionable, ask yourself these questions about your dealings with your own insurance company (UM/UIM/MedPay):

- The Ghosting: Have more than 15 days passed since you sent a letter or email without a response?

- The Mystery Denial: Did they deny your claim without giving a specific reason or citing the specific policy page?

- The Lowball: Did they offer you $5,000 for a surgery that clearly costs $50,000?

- The Paper Chase: Are they asking for the same documents over and over again to delay paying?

- The Shift: Did they try to change the policy limits or coverage details después, you filed the claim?

If you answered yes to any of these, you aren’t just having a customer service issue. You are likely a victim of Bad Faith. You don’t have to face them alone. Call DK Law for a free consultation today.

DK All the Way

Desde su primer contacto hasta recibir su compensación, estamos con todos all the way.

Agende una consulta gratuita

Reciba asesoría legal experta sin ningún costo.

En DK Law estamos a su lado — all the way.

¡Agende hoy su consulta gratuita con nuestros expertos!

El tiempo es importante después de un accidente

Cuanto antes hables con un abogado después de un accidente, más sólido puede ser su reclamo. Actuar pronto ayuda a preservar la evidencia y a proteger sus derechos.

No ganamos, no cobramos | Disponible 24/7